Please note that the items listed below are not exhaustive and that other factors may affect the comparisons for FY 2022 versus the same period last year.

This Aide-Memoire contains certain statements that are, or may be deemed to be, "forward-looking statements" (including for purposes of the safe harbour provisions for forward-looking statements contained in Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934). Forward-looking statements give Haleon's expectations and projections, as of the date such statements are made, about future events, including strategic initiatives and future financial condition and performance, and so Haleon's actual results may differ materially from what is expressed or implied by such forward-looking statements. Please see the "Cautionary statement note regarding forward-looking statements" sections of the Q3 Trading Statement and the H1 2022 results regarding the forward-looking statements from such documents that are extracted in this aide-memoire. Please also read the definitions and reconciliations for non-IFRS measures on pages 8-12 of the Q3 Trading Statement, pages 39-45 of the H1 2022 results, and in Haleon's Registration Statement on Form 20-F.

Outlook

In the Q3 Trading Statement, we provided an update on revenue and adjusted operating margin guidance for FY 2022:

Revenue

- “FY22 organic revenue growth expected at 8.0-8.5%.”

- “FY guidance implies about 1.5-3.5% growth in Q4” as shared at Q3 conference call on 10 November 2022.

Adjusted operating margin

- At H1 Results we guided to FY22 adjusted operating profit margin slightly down at constant currency. Operational performance remains as expected with pricing and increased efficiencies fully offsetting inflationary pressures, albeit we now would expect an increase in the adverse transactional FX impact from recent currency movements of up to 30bps. Adjusted operating margin in FY22 is now expected to be slightly above last year at actual exchange rates (FY21: 22.8%), given recent favourable translational FX movements.” (Assuming spot rates as at 31 October 2022 are sustained).

A reminder of other FY2022 guidance, as shared with H1 2022 results:

- Adjusted effective tax rate expected to be at the lower end of the 22-23% range

- Net interest expense expected at £0.2bn

- Net capex guidance expected at c.3% sales.

- Separation and Admission costs expected to be approximately £0.5bn (at spot rates as at the time of the publication of H1 2022 results) between FY2022 and FY2024, with 80% of costs incurred in FY2022, and the balance split across FY2023 and FY 2024. Admission costs expected to be just over £0.1bn.

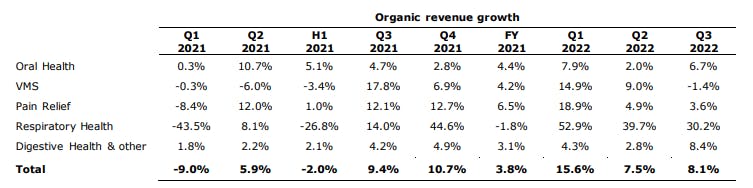

Category performance comments

- Oral Health – H1 2022 indicative of trends this year given Q2 2022 was adversely impacted by impact of Covid in China. Q3 2022 organic growth of +6.7% reflected China starting to come back as lockdown restrictions began to lift in some cities.

- VMS – During H2 2021, Haleon brought incremental supply capacity on stream for VMS which benefitted organic growth in the second half of last year with organic growth in Q3 and Q4 2021 at 17.8% and 6.9% respectively. During H2 2022, Haleon cycled over those comparatives. In addition, Tobias Hestler noted on the Q3 2022 analyst/investor call that “in recent months, Emergen-C demand has been skewed towards times of Covid demand.”

- Pain Relief - Comparatives for organic growth are similar through Q3 and Q4 2021 at 12.1% and 12.7% respectively. Organic growth for Pain Relief was 11.7% for H1 2022 and 4.9% and 3.6% in Q2 and Q3 2022 respectively.

- Respiratory Health - There were some benefits seen in Q3 2022 from advanced cold and flu purchasing ahead of the season. In Q4 2021, cold and flu sales were almost back to pre-pandemic levels. That said, recent media commentary and data indicates a strong cold and flu season is underway, 1 though bear in mind that Q4 is the start of the season and incidences of cold and flu can be volatile.

- Digestive Health and Other – Organic revenue growth has historically been low single digit. During Q3, organic growth was 8.4% which would suggest some sell in ahead of Q4.

Geographic regions

- North America – As noted during the Q3 2022 analyst/investor call, on 1st October 2021, Haleon implemented mid-to-high single digit price increases on 50% of the US categories. During Q4, we will have lapped this.

Other comments for consideration

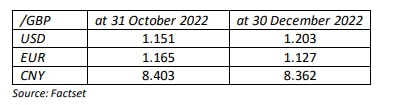

- Foreign exchange – As a reminder, the most recent guidance included in the Q3 Trading Statement was based on FX rates as at 31 October 2022. Spot rates for the three most important currencies for Group revenue is below.

- Net Debt – Net debt shared at the end of Q3 was £10,784m, which was based on FX rates of USD/GBP 1.107 and Euro/GBP 1.134 as at 30 September 2022.

- Interest costs in FY23 – At H1 results and on the Q3 trading statement call, Tobias Hestler flagged that the £200 million net interest cost guidance includes a £40 million offset from income from the on-lending of the bonds between March and 18th July to GSK and Pfizer. This £40 million income will not be repeated in 2023. In addition, as a reminder in 2022, we had bond debt for nine months only, and 2023 will reflect a full year of holding the bond debt. Finally, as a reminder, 20% of Haleon debt is floating, and the interest rate environment has changed since March 2022 when we issued the bonds.

Prior year comparatives and recent performance

ENDS

Enquiries

Sonya Ghobrial +44 7392 784784

Rakesh patel +44 7552 484646

Emma White +44 7792 750133

Email: [email protected]

1 - Source: Financial Times, 4 January 2023; CDC data